A friend asked for a quick list, so here goes:

UCLA's excellent resources to help you learn and use Stata

Another great collection of Stata Resources by Park Hun Myoung, as well as a stata command cheat-card

London School of Economics Stata Resources

Syracuse University's Stata tutorial

Program in Statistics and Methodology by the pol sci's at Ohio State University

Duke Stata tutorials

Monday, 29 September 2008

Sunday, 28 September 2008

Social capital formation in rats

[...] we show experimentally that cooperative behavior of female rats is influenced by prior receipt of help, irrespective of the identity of the partner. Rats that were trained in an instrumental cooperative task (pulling a stick in order to produce food for a partner) pulled more often for an unknown partner after they were helped than if they had not received help before.

The paper, published in PLoS Biology, is free to access. With the exception of direct reciprocity (the 'you've been nice to me, I'll be nice to you' type), no other mechanism for reciprocity had ever been demonstrated in nonhuman animals before.

'Altruistic behavior by previous social experience irrespective of partner identity' is fundamental to human society, and perhaps the single behaviour economic theory most struggles with.

Bailout tidbits

In case you missed it, Friday saw a hell of a meeting:

The intense discussions reportedly saw US Treasury Secretary Henry Paulson literally down on one knee, begging Ms Pelosi to help push through the bail-out package.

It looks like economists may have had something to do with the plan bein' stalled and all:

Republican Senator Richard Shelby moments ago on CNN explaining why the tentative deal reached earlier today is bunk:

"If 200 of our economists say the plan is flawed we should listen to them."

Here's the statement by the actually 192 economists.

And last but not least, Greg Mankiw's smart friend discovers a free lunch - go no further than point 1.

Thursday, 25 September 2008

Friday Special 73

Photos That Changed The World (explicit picture warning)

Photos That Changed The World (explicit picture warning)Twelve canoes: We are the first people of our lands.

You couldn't ski to save yourself - perfect for a Friday lunch break

Wednesday, 24 September 2008

Why $700 billion?

I was wondering about that. Zubin Jelveh has the answer:

Nice.

[...] There are roughly $14 trillion in outstanding residential and commercial mortgages and five percent is also roughly the loss rate on those categories, he added. Five percent of $14 trillion is = $700 billion.

Nice.

"It's not science," Bernanke said.

Monday, 22 September 2008

Wronging rights

Kate has a B.A. in Genocide from NYU's Gallatin School. Amanda has a Masters Degree in Violence, Conflict, and Development Studies from SOAS at the University of London.

These girls have some seriously wicked education, and they author the highly recommended wronging rights blog. Their special skills: crimes against humanity, modern warfare, and the social construction of atrocity. It's a delight to read.

Postscript: As a bonus, the top post right now comments on yet another horrid BBC news story - and as loyal readers of this blog know, I NEVER get tired of stories pointing out how abysmally bad the BBC is and imply I should be getting my license fee back.

Sunday, 21 September 2008

Losing money to avoid the risk of losing money

There are two main reasons people don't want government interfering in private markets:

1. The rule of law. No-one can be referee and player at the same time, and government officials should not be allowed to use their discretion to benefit one player over another.

With the Paulson plan, not only will there be discretionary action on a vast scale, but it also looks like there will be a minimal degree of accountability. This is not specific to the current plan however: any 'solution to the crisis' requires discretionary, arbitrary actions by the Treasury and Fed.

2. Government is inefficient. It is likely to make a mess of things and waste taxpayer money, so if something can be handled by the private sector it should be.

What I find funny with the Paulson plan is that instead of doing something to address this worry, it actually guarantees that taxpayers' money will be wasted. The fund is limited to buying worthless securities, so it doesn't even allow the possibility the taxpayer might turn a profit or even minimise the loss. It boils down to preferring to lose money instead of running a risk of losing money.

And what makes this even more remarkable is that the current environment is the best possible for government to actually make money by investing in financial markets. Following standard commentary, the biggest problem right now is not that there are gigantic losses in the system, but rather a lack of liquidity and a lack of trust. Government is the unique institution right now that enjoys an abundance of both, and in any economic system whoever controls the scarce resource is amply rewarded.

A plan along those lines, albeit one which I think could be improved, is described here. The Economist blogger's reaction is telling:

The Zingales plan also has much to recommend it, although it wouldn't be my first best option.

For my take on the long-term solution to the problems in the finance industry, tune in later this week.

Many (other) serious people think the Paulson plan sucks: see Naked Capitalism, Politico, and of course Tyler Cowen and Greg Mankiw.

1. The rule of law. No-one can be referee and player at the same time, and government officials should not be allowed to use their discretion to benefit one player over another.

With the Paulson plan, not only will there be discretionary action on a vast scale, but it also looks like there will be a minimal degree of accountability. This is not specific to the current plan however: any 'solution to the crisis' requires discretionary, arbitrary actions by the Treasury and Fed.

2. Government is inefficient. It is likely to make a mess of things and waste taxpayer money, so if something can be handled by the private sector it should be.

What I find funny with the Paulson plan is that instead of doing something to address this worry, it actually guarantees that taxpayers' money will be wasted. The fund is limited to buying worthless securities, so it doesn't even allow the possibility the taxpayer might turn a profit or even minimise the loss. It boils down to preferring to lose money instead of running a risk of losing money.

And what makes this even more remarkable is that the current environment is the best possible for government to actually make money by investing in financial markets. Following standard commentary, the biggest problem right now is not that there are gigantic losses in the system, but rather a lack of liquidity and a lack of trust. Government is the unique institution right now that enjoys an abundance of both, and in any economic system whoever controls the scarce resource is amply rewarded.

A plan along those lines, albeit one which I think could be improved, is described here. The Economist blogger's reaction is telling:

I get the feeling that a bigger hurdle to the latter plan than any real concern would be a gut Congressional reaction against the government taking equity stakes in a broad array of American corporations.

The Zingales plan also has much to recommend it, although it wouldn't be my first best option.

For my take on the long-term solution to the problems in the finance industry, tune in later this week.

Many (other) serious people think the Paulson plan sucks: see Naked Capitalism, Politico, and of course Tyler Cowen and Greg Mankiw.

3 year old saves mother's life

Incredible:

A three-year-old boy came to his mother's rescue by dialling 999 after she had an epileptic fit.

Jack Thomson called the emergency services from his mum's mobile phone. When the line went dead he found another phone and dialled again.

Here's the video report.

Quis custodiet ipsos custodes?

It is enough to say that for 6 of the last 13 years, the Secretary of Treasury was a Goldman Sachs alumnus. But, as financial experts, this silence is also our responsibility. Just as it is difficult to find a doctor willing to testify against another doctor in a malpractice suit, no matter how egregious the case, finance experts in both political parties are too friendly to the industry they study and work in.

This is from the the truly excellent 2-page essay by Luigi Zingales on why the Paulson plan sucks. He is right: no matter how easily you can switch your hats around, you may find it difficult to be harsh to the people and companies you spent your career with. Did Margaret Thatcher hail from a long line of coal-miners?

Manchester United's new shirt

Old Manchester United shirt:

New Manchester United shirt, to reflect change of sponsor:

New Manchester United shirt, to reflect change of sponsor:

And from the same loyal reader, I have no idea if this is true but it still is hillarious:

New Manchester United shirt, to reflect change of sponsor:

New Manchester United shirt, to reflect change of sponsor:

And from the same loyal reader, I have no idea if this is true but it still is hillarious:

Bloomberg reports that Lehman's Brothers' Canary Wharf landlord prudently insured the firm's rent in case Lehman ever had difficulty paying up. It looked dodgy there for a moment, though, as the policy was taken out with AIG...

Thursday, 18 September 2008

Friday Special 72

Probability of Barack Obama win and Expected Electoral Votes

Goog-411: Another attempt to making our lives easier

Tuesday, 16 September 2008

The destruction that Lehman wrought

Empires came crumbling down, blood flowed on the trading floors and the real economy quickly headed for the Great Depression mark II. The collapse of Lehman Brothers led to a true Black Week, as predicted by numerous self-serving bankers.

Only it didn't.

The Dow fell from 11260 four days ago to 11060 yesterday - that's 200 points, or 1.8%. When future dictionaries define 'disaster', they will not be displaying this picture by means of example:

(Source: Yahoo finance)

(Source: Yahoo finance)

Now, the worse is not necessarily over, and markets might yet crash as a direct result of this week's events. There is still a not-so-reassuringly-low probability this blogger will have to eat his words in the not so distant future. But so far it looks like Lehman's demise caused no more than a shrug.

It really is impressive how quickly the lessons of Bear Stearns were not only understood but also put to action by the bankers (be sinister and wait long enough, and the Treasury will give you a bank for free.) Yet, it is even more impressive how the government put an end to the emerging orthodoxy.

A proud week for everyone fighting on the taxpayer's side. Public officials, I salute you!

Only it didn't.

The Dow fell from 11260 four days ago to 11060 yesterday - that's 200 points, or 1.8%. When future dictionaries define 'disaster', they will not be displaying this picture by means of example:

(Source: Yahoo finance)

(Source: Yahoo finance)Now, the worse is not necessarily over, and markets might yet crash as a direct result of this week's events. There is still a not-so-reassuringly-low probability this blogger will have to eat his words in the not so distant future. But so far it looks like Lehman's demise caused no more than a shrug.

It really is impressive how quickly the lessons of Bear Stearns were not only understood but also put to action by the bankers (be sinister and wait long enough, and the Treasury will give you a bank for free.) Yet, it is even more impressive how the government put an end to the emerging orthodoxy.

A proud week for everyone fighting on the taxpayer's side. Public officials, I salute you!

Best argument for creationism, ever

No, not this one. This reminds me too much of celestial teapots and the fact that a strong prior will get you anywhere (and you can't have science without priors). Thucydides would have been appalled by this sophistry. I'm talking about this one:

We have no reason to accept knowledge that disatisfies us. You should believe what pleases you.

Just don't try this with gravity.

The materialist explanation of the creation has nothing to offer - if we came from nothing and go into nothing, then that encourages people to lead reckless and materialistic lifestyles.

Evolution is a world-view that leads to futility. It's no wonder people are dissatisfied with it.

We have no reason to accept knowledge that disatisfies us. You should believe what pleases you.

Just don't try this with gravity.

What happens when we die?

A number of recent scientific studies carried out by independent researchers have demonstrated that 10-20 per cent of people who go through cardiac arrest and clinical death report lucid, well structured thought processes, reasoning, memories and sometimes detailed recall of events during their encounter with death.

Here is more on the World's Largest-Ever Study of Near Death Experiences. This is interesting stuff:

“Contrary to popular perception,” Dr Parnia explains, “death is not a specific moment. It is a process that begins when the heart stops beating, the lungs stop working and the brain ceases functioning – a medical condition termed cardiac arrest, which from a biological viewpoint is synonymous with clinical death.

“During a cardiac arrest, all three criteria of death are present. There then follows a period of time, which may last from a few seconds to an hour or more, in which emergency medical efforts may succeed in restarting the heart and reversing the dying process. What people experience during this period of cardiac arrest provides a unique window of understanding into what we are all likely to experience during the dying process.”

During the AWARE study, doctors will use sophisticated technology to study the brain and consciousness during cardiac arrest. At the same time, they will test the validity of out of body experiences and claims of being able to ‘see’ and ‘hear’ during cardiac arrest.

Monday, 15 September 2008

Dealing with fanmail

Science fiction master Robert Heinlein engineered his own nerdy solution to a problem common to famous authors: how to deal with fan mail.

In the days before the internet, Heinlein's solution was fabulous. He created a one page FAQ answer sheet -- minus the questions. Then he, or rather his wife Ginny, checked off the appropriate answer and mailed it back. While getting a form letter back might be thought rude, it was much better than being ignored, and besides, the other questions you did not ask were also answered!

From CT2, via Statistical Modeling. The actual letter is brilliant:

Inequality, poverty, or something else?

The 'human cost' of the collapse of Lehman Brothers:

Many serious people believe that what really matters is helping people in poverty; others point out that people have preferences for the degree of inequality as well, beyond making sure the weakest in society can enjoy a certain minimum standard of living.

But this story shows there's something else at play too: being paid what is perceived 'fair', and changes in relative status. Hence our sympathy for the managing director who is losing his bonus, and our dislike of the burglar, as well as our sadness for the fallen rockstar and deposed King.

Andy Bevan, 27, who works in equity derivative finance, was more upbeat.

He said he had been given the "official word" at about midday.

"It is what it is," he said. "But I am lucky - I don't have any dependants or a mortgage to worry about. I feel sorry for the managing directors - they were paid about 50% of their bonus in stock, that's been written off."

Many serious people believe that what really matters is helping people in poverty; others point out that people have preferences for the degree of inequality as well, beyond making sure the weakest in society can enjoy a certain minimum standard of living.

But this story shows there's something else at play too: being paid what is perceived 'fair', and changes in relative status. Hence our sympathy for the managing director who is losing his bonus, and our dislike of the burglar, as well as our sadness for the fallen rockstar and deposed King.

The WSJ is copying us!

Check this out, from Kids Prefer Cheese:

WSJ: "Divided Government is Best for the Market"

Loyal Bluematter. readers will of course remember that this type of analysis was pioneered here, in a seminal post investigating what more daughters do to a President.

WSJ: "Divided Government is Best for the Market"

...since 1948, the stock market has done better under Democratic presidents (15.6%) than Republican ones (11.1%).

But it's not so simple... First, not all Democrats act like Democrats, and not all Republicans act like Republicans. John F. Kennedy, for example, was an enthusiastic supply-side tax cutter, and George H.W. Bush raised taxes. Bill Clinton promoted free trade, and Richard Nixon imposed wage and price controls.

If you assign those four presidents to the opposite party based on that -- make the two Democrats into Republicans and the two Republicans into Democrats -- the numbers completely reverse. Now stocks average 14.7% under Republicans and only 10.5% under Democrats.

In fact, it turns out that if you do just one single switch -- if you make Richard Nixon into a Democrat -- it's enough to reverse the numbers."

Loyal Bluematter. readers will of course remember that this type of analysis was pioneered here, in a seminal post investigating what more daughters do to a President.

Thursday, 11 September 2008

Friday Special 71

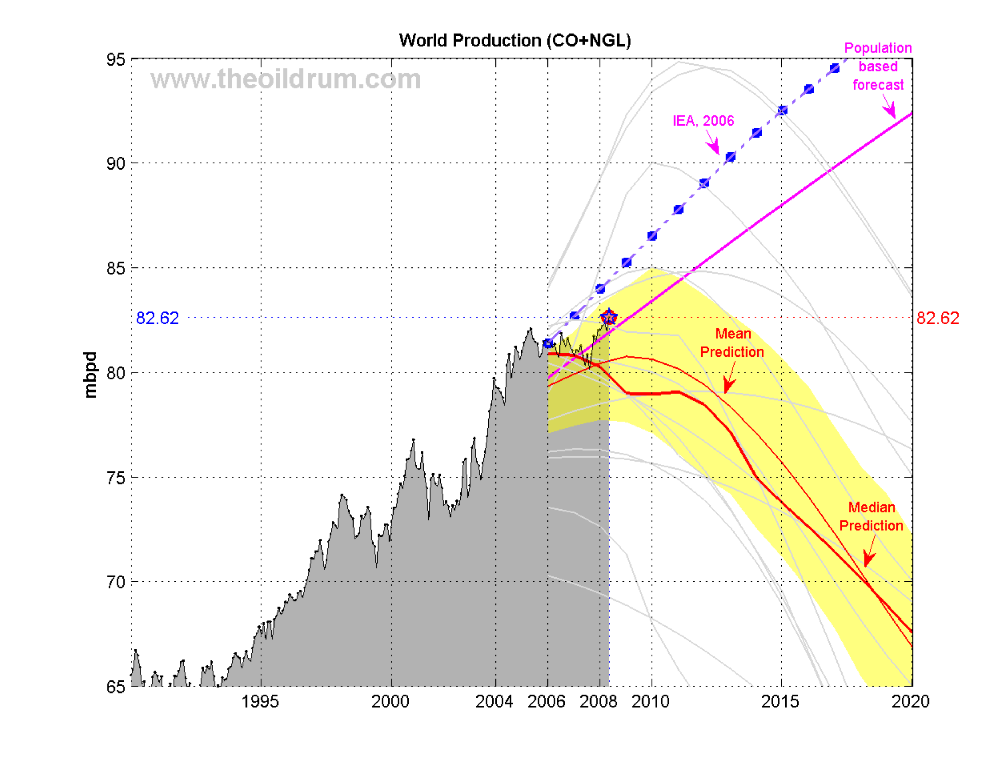

World oil production forecasts

World oil production forecastsThe highly effective search egnine SearchMe is most likely the best you have ever used

REI travel adventure is to desire, to experience, to seize

A thought that has been on our minds this week

On the art of street illusion

Play with the spider

Wednesday, 10 September 2008

On externalities and Pigouvian taxation

The issue

Most people don't know how to deal with an externality, and don't understand the purpose of Pigouvian (not Pigovian - see footnote) taxes. 'Most people' is more likely than not to include you too.

Shock value

The extent to which people change their actions as a result of pigouvian taxation is irrelevant. So, a pigouvian tax on carbon emmissions is the best response to global warming, even if it does not lead to any reductions in carbon emissions.

The snappy part

An externality is generated when I do not take into account the full social costs of my actions when making decisions. In other words, I do something I like which you don't, but because I don't care about your feelings I end up doing it too much.

For an externality to create problems, two things must be going on:

a. no clearly established property rights (am I entitled to polluting or are you entitled to a clean environment?)

b. trade between the holder of the property rights and the non-holder is not possible (i.e. I can't compensate you to allow me to pollute if you are entitled to a clean environment, or you can't pay me to not pollute if I am entitled to pollute).

Let's stick with carbon emmissions. Property rights are well established: they are held by governments, and they can choose to represent the rights of all people of the world, the fauna and the flora of the world and generations yet unborn as they see fit. So no problems there.

The means to trade are also present: enter pigouvian taxation.

Now, most people think that a pigouvian tax ought to be imposed to reduce pollution, full stop. If the pigouvian tax has only a small effect on carbon emmisions, the thinking goes, then the pigouvian tax has 'failed' and other measures ought to be taken, namely non-price restrictions (e.g. banning carbon emmissions above a certain level, restricting the supply of oil, etc).

This is wrong. The degree to which the production of carbon emmissions changes is irrelevant. As long as your pigouvian tax equates the private to the social costs, you are in the best possible world. If you don't agree, then your problem lies with the initial allocation of property rights or with the distribution of the pigouvian tax revenue or with democracy itself, not with correcting for the externality in the world in which we live in.

The only 'problem' stemming from an 'uncorrected' externality is inefficiency, and the best way to deal with that inefficiency is to apply an appropriate pigouvian tax. Any perceived problems beyond inefficiency should not be addressed in the context of 'correcting' the externality.

Illustrative example - post starts getting boring from here onwards

I like driving my car around your garden. You like your garden to be car-free. I produce an externality in that my private actions affect your welfare.

Possibility A: You own the garden. If driving my car is worth more to me than having a car-free garden is worth to you, I can pay you so that you let me drive in your garden. If not, I don't pay you and you have a car-free garden. That's Pareto efficiency; you can't make anyone better off without making someone worse off.

Possibility B: I own the garden. If driving my car is worth less to me than having a car-free garden is worth to you, you can pay me so that I don't drive around. If not, you don't pay me and I keep driving around. That's Pareto efficiency again.

Now, substitute 'you tax me' for 'I pay you' and you can relate this to the rest of the post.

And if you believe that the outcome is not socially optimal, then you really have a problem with the initial allocation of property rights, not with the means by which the externality is handled. Voicing your concerns now doesn't make sense; your grievances have nothing to do with the externality we discuss here.

What you believe is that the initial allocation of wealth is wrong on grounds of fairness. The way to combat this is by moving some wealth from the garden guy to the car guy or vice versa. The tax/subsidy on car-driving is not really central to your argument.

Now you may want to skip to the footnote; for the remainder of the post I simply repeat everything I said earlier in an irritating manner

Tyler Cowen, who easily ranks amongst the top thinkers we have on social and economics issues, shocked me with this post. (One of the most powerful economists in the world also shocked me for similar reasons in a talk I attended recently, but I expected more from Tyler).

Tyler's post discusses whether it makes sense to drill in Alaska (the ANWR), and here's an excerpt:

There can be no 'general global warming case'. Fighting global warming is a means to an end, not an end in itself. I don't want a guarantee the stuff won't be pumped away, I just want those who suffer from the externality (be it non-users of fuel, Africans, wild animals or children yet to be born) to be adequately compensated by those who benefit from burning fuel. Remember the Coase theorem! The Pigouvian tax can be seen as the result of the bargaining between the different social groups with their different preferences. A crude instrument, I know, but the problems associated with establishing the optimal Pigouvian tax rate do not go away when considering non-price restrictions (and what is banning something if not an extremely large Pigouvian tax, implying an extremely large externality?).

If you are arguing against developing ANWR 'because supply restrictions can be far more effective than a Pigou tax' then why don't you also make a 'general global warming case' against developing Africa (you could use the resources to install solar panels), against reading books (you could use the resources spent reading them to pay people not to use fuel) and against living and breathing (you produce carbon emmissions)?

Again, the point is not to restrict fossil fuel use for its own sake, or even to raise the price because we want less consumed for the fun of it. All a Pigouvian tax has to do is equate the private with the social costs of polluting; if that is the case, whatever carbon emmissions there are at equilibrium represent the optimal amount.

Why does this misunderstanding about externalities and pigouvian taxation persists? I can only speculate. Firstly, standard textbook treatments do not bother with where the funds go (beyond stressing that, to get a neat solution, they are not to be redistributed back to the externality generators - polluters). Secondly, the sloppy ('common sense') thinking often applied requires that we should be looking to eliminate anything 'bad' such as carbon emissions, not merely restricting it to socially optimal levels.

The footnote

Pigovian is the most funny Americanism there is. You can spell labour 'labor' and behaviour 'behavior', but the guy wasn't called Pigo.

Most people don't know how to deal with an externality, and don't understand the purpose of Pigouvian (not Pigovian - see footnote) taxes. 'Most people' is more likely than not to include you too.

Shock value

The extent to which people change their actions as a result of pigouvian taxation is irrelevant. So, a pigouvian tax on carbon emmissions is the best response to global warming, even if it does not lead to any reductions in carbon emissions.

The snappy part

An externality is generated when I do not take into account the full social costs of my actions when making decisions. In other words, I do something I like which you don't, but because I don't care about your feelings I end up doing it too much.

For an externality to create problems, two things must be going on:

a. no clearly established property rights (am I entitled to polluting or are you entitled to a clean environment?)

b. trade between the holder of the property rights and the non-holder is not possible (i.e. I can't compensate you to allow me to pollute if you are entitled to a clean environment, or you can't pay me to not pollute if I am entitled to pollute).

Let's stick with carbon emmissions. Property rights are well established: they are held by governments, and they can choose to represent the rights of all people of the world, the fauna and the flora of the world and generations yet unborn as they see fit. So no problems there.

The means to trade are also present: enter pigouvian taxation.

Now, most people think that a pigouvian tax ought to be imposed to reduce pollution, full stop. If the pigouvian tax has only a small effect on carbon emmisions, the thinking goes, then the pigouvian tax has 'failed' and other measures ought to be taken, namely non-price restrictions (e.g. banning carbon emmissions above a certain level, restricting the supply of oil, etc).

This is wrong. The degree to which the production of carbon emmissions changes is irrelevant. As long as your pigouvian tax equates the private to the social costs, you are in the best possible world. If you don't agree, then your problem lies with the initial allocation of property rights or with the distribution of the pigouvian tax revenue or with democracy itself, not with correcting for the externality in the world in which we live in.

The only 'problem' stemming from an 'uncorrected' externality is inefficiency, and the best way to deal with that inefficiency is to apply an appropriate pigouvian tax. Any perceived problems beyond inefficiency should not be addressed in the context of 'correcting' the externality.

Illustrative example - post starts getting boring from here onwards

I like driving my car around your garden. You like your garden to be car-free. I produce an externality in that my private actions affect your welfare.

Possibility A: You own the garden. If driving my car is worth more to me than having a car-free garden is worth to you, I can pay you so that you let me drive in your garden. If not, I don't pay you and you have a car-free garden. That's Pareto efficiency; you can't make anyone better off without making someone worse off.

Possibility B: I own the garden. If driving my car is worth less to me than having a car-free garden is worth to you, you can pay me so that I don't drive around. If not, you don't pay me and I keep driving around. That's Pareto efficiency again.

Now, substitute 'you tax me' for 'I pay you' and you can relate this to the rest of the post.

And if you believe that the outcome is not socially optimal, then you really have a problem with the initial allocation of property rights, not with the means by which the externality is handled. Voicing your concerns now doesn't make sense; your grievances have nothing to do with the externality we discuss here.

What you believe is that the initial allocation of wealth is wrong on grounds of fairness. The way to combat this is by moving some wealth from the garden guy to the car guy or vice versa. The tax/subsidy on car-driving is not really central to your argument.

Now you may want to skip to the footnote; for the remainder of the post I simply repeat everything I said earlier in an irritating manner

Tyler Cowen, who easily ranks amongst the top thinkers we have on social and economics issues, shocked me with this post. (One of the most powerful economists in the world also shocked me for similar reasons in a talk I attended recently, but I expected more from Tyler).

Tyler's post discusses whether it makes sense to drill in Alaska (the ANWR), and here's an excerpt:

2. There is a general global warming case against developing the resource. Note that supply restrictions can be far more effective than a Pigou tax. A Pigou tax doesn't guarantee the stuff won't be pumped anyway, albeit at lower profit.

There can be no 'general global warming case'. Fighting global warming is a means to an end, not an end in itself. I don't want a guarantee the stuff won't be pumped away, I just want those who suffer from the externality (be it non-users of fuel, Africans, wild animals or children yet to be born) to be adequately compensated by those who benefit from burning fuel. Remember the Coase theorem! The Pigouvian tax can be seen as the result of the bargaining between the different social groups with their different preferences. A crude instrument, I know, but the problems associated with establishing the optimal Pigouvian tax rate do not go away when considering non-price restrictions (and what is banning something if not an extremely large Pigouvian tax, implying an extremely large externality?).

If you are arguing against developing ANWR 'because supply restrictions can be far more effective than a Pigou tax' then why don't you also make a 'general global warming case' against developing Africa (you could use the resources to install solar panels), against reading books (you could use the resources spent reading them to pay people not to use fuel) and against living and breathing (you produce carbon emmissions)?

3. The Pigouvian case against developing ANWR makes sense only if we are taking other systematic actions to raise the price of fossil fuels and restrict fossil fuel use.

Again, the point is not to restrict fossil fuel use for its own sake, or even to raise the price because we want less consumed for the fun of it. All a Pigouvian tax has to do is equate the private with the social costs of polluting; if that is the case, whatever carbon emmissions there are at equilibrium represent the optimal amount.

Why does this misunderstanding about externalities and pigouvian taxation persists? I can only speculate. Firstly, standard textbook treatments do not bother with where the funds go (beyond stressing that, to get a neat solution, they are not to be redistributed back to the externality generators - polluters). Secondly, the sloppy ('common sense') thinking often applied requires that we should be looking to eliminate anything 'bad' such as carbon emissions, not merely restricting it to socially optimal levels.

The footnote

Pigovian is the most funny Americanism there is. You can spell labour 'labor' and behaviour 'behavior', but the guy wasn't called Pigo.

Tuesday, 9 September 2008

A lesson in statistics

Andrew Gelman:

This is a big topic for another day - the day I start posting on my main area of expertise, econometrics - but these are words worth pondering.

[...] when he talks with people about statistical procedures, engineers focus on the algorithm being applied to the data, whereas statisticians are always thinking about the psychology of the person doing the analysis.

This is a big topic for another day - the day I start posting on my main area of expertise, econometrics - but these are words worth pondering.

Sunday, 7 September 2008

The moral content of economic terminology in the popular press: A guide

Foreign direct investment (inbound): Good

Current account deficit: Bad

Trade deficit: Catastrophic

Capital account deficit: Not used. Presumably bad.

Weak national currency: Bad

Exports: Good

Imports: Bad

Rising house prices: Good

Falling house prices: Bad

Affordable houses: Good

Unaffordable houses: Bad

Free trade: Neutral

Unfettered free trade: Bad

Fair trade: Good

Outsourcing: Evil

Buying local produce: Divine

Pay rises: Good

Low interest rates: Good

Inflation: Bad

Communism: Very Bad

Socialism: Bad

Capitalism: Bad

Current account deficit: Bad

Trade deficit: Catastrophic

Capital account deficit: Not used. Presumably bad.

Weak national currency: Bad

Exports: Good

Imports: Bad

Rising house prices: Good

Falling house prices: Bad

Affordable houses: Good

Unaffordable houses: Bad

Free trade: Neutral

Unfettered free trade: Bad

Fair trade: Good

Outsourcing: Evil

Buying local produce: Divine

Pay rises: Good

Low interest rates: Good

Inflation: Bad

Communism: Very Bad

Socialism: Bad

Capitalism: Bad

Two different societies

My two home nations are very different, and it's reflected in the tax code:

In the UK, inheritance tax is applicable (at a declining rate) for transfers made up to seven years before death. Transfers of assets from a parent to the children prior to that are not taxed, and also note that there is a very significant tax-free allowance (£600,000). Nevertheless, inheritance tax raises roughly £3.5 billion a year.

In Greece, the tax on transfers of assets from parents to kids is waged at virtually the same level as inheritance tax - if that was not the case, inheritance tax would probably raise no revenue at all. In fact, a lot of families transfer assets two generations down the line (i.e. grandparents to grandchildren) to avoid paying too much tax, and they usually do so long before death (to avoid higher income tax charges).

In the UK, inheritance tax is applicable (at a declining rate) for transfers made up to seven years before death. Transfers of assets from a parent to the children prior to that are not taxed, and also note that there is a very significant tax-free allowance (£600,000). Nevertheless, inheritance tax raises roughly £3.5 billion a year.

In Greece, the tax on transfers of assets from parents to kids is waged at virtually the same level as inheritance tax - if that was not the case, inheritance tax would probably raise no revenue at all. In fact, a lot of families transfer assets two generations down the line (i.e. grandparents to grandchildren) to avoid paying too much tax, and they usually do so long before death (to avoid higher income tax charges).

Thursday, 4 September 2008

Friday Special 70

Panoramic Snake River view in Grand Teton National Park, Wyoming

Panoramic Snake River view in Grand Teton National Park, WyomingLaunched today: GeoEye - to map, monitor, and measure the Earth

Seven Revolutions: What will the world look like in 2025?

Google unveils anticipated Chrome web browser

The Homer Simpson Euro

The art of the hobo nickel - carving new imagery into currency.A man in Spain recently found a Euro coin with Homer Simpson carved into what was previously the bust of Spanish King Juan Carlos. Reuters link

HT Blogadilla - (hey guys, I love your layout!). Here's more currency from the Original Hobo Nickel Society.

Wednesday, 3 September 2008

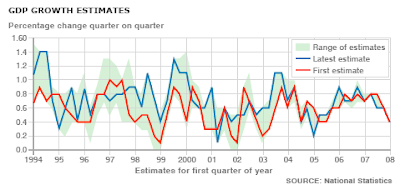

How reliable are GDP estimates?

Not very. The graph depicts UK data - note that the 'latest estimate' is our best estimate but, of course, by no means the true value:

Thanks to Michael Blastland for putting the graph together. Here's his fifth article on the ways in which the media abuse statistics, scroll down the page for links to the other four.

Thanks to Michael Blastland for putting the graph together. Here's his fifth article on the ways in which the media abuse statistics, scroll down the page for links to the other four.

Thanks to Michael Blastland for putting the graph together. Here's his fifth article on the ways in which the media abuse statistics, scroll down the page for links to the other four.

Thanks to Michael Blastland for putting the graph together. Here's his fifth article on the ways in which the media abuse statistics, scroll down the page for links to the other four.

Prison and TB

Using longitudinal TB and cross-sectional multidrug-resistant TB data for 26 eastern European and central Asian countries, we examined whether and to what degree increases in incarceration account for differences in population TB and multidrug-resistant TB burdens.

We find that each percentage point increase in incarceration rates relates to an increased TB incidence of 0.34%.

Net increases in incarceration account for a 20.5% increase in TB incidence or nearly three-fifths of the average total increase in TB incidence in the countries studied from 1991 to 2002.

The paper (gated) is here.

Tuesday, 2 September 2008

The voice dies

Don LaFontaine passed away, at the age of 68. As a kid, I often wondered how different the world -or at least the cinema- would be without him.

He was 'the narrator guy in all the movie trailers'. Here's a great youtube clip.

He was 'the narrator guy in all the movie trailers'. Here's a great youtube clip.

Fun with statistics, "which Palin is the mother?" edition

Well, Sarah, I'm calling you a liar. And not even a good one. Trig Paxson Van Palin is not your son. He is your grandson.

The Daily Kos has an 'interesting' story claiming that Sarah Palin's youngest son, who has been diagnosed with Down's syndrome, is really her daughter's son. There is much evidence presented, mainly consisting of pictures where certain bellies appear to be too large while others too small. But statistics deliver the killer argument:

The final point of interest is that Trig Palin has been diagnosed with Down's syndrome (aka trisomy 21). This is an interesting point, as chances of having offspring with Down's Syndrome increases from under 1% to 3% after a mother reaches the age of 40. However, 80% of the cases of Down's Syndrome are in mother's (sic) under the age of 35, through sheer quantities of births in this age group.

And of course, 99% of deaths are not due to suicide, so killing yourself is safe!

Thanks to Scatterplot for the pointer.

Obama on the beach

They don't come cuter than that! For many more pictures & a family bio, check out Obama's scrapbook.

Subscribe to:

Comments (Atom)